Fill Out a Valid New Mexico Pit Rc Template

The New Mexico PIT-RC form is an integral document for residents looking to navigate their financial obligations and benefits under state law, specifically for individuals who qualify for one or more refundable rebates and credits within the region. This form, meticulously crafted to finalize the rebate and credit schedule, is customized to be included alongside the Personal Income Tax Return, Form PIT-1, substantially simplifying the process for taxpayers. It constitutes a series of sections, each dedicated to different qualifiers and types of rebates or credits, such as the Property Tax Rebate for seniors, the New Mexico Child Day Care Credit, and the Low Income Property Tax Rebate exclusive to residents of Los Alamos or Santa Fe County among others. Moreover, it delves into the calculation of modified gross income to establish eligibility for said benefits, emphasizing the importance of accuracy in reporting income and household information. The form also outlines specifics regarding additional tangible benefits, demonstrating New Mexico’s commitment to supporting its residents through various financial mechanisms. By completing the PIT-RC form with attention to the detailed requirements and instructions provided, eligible New Mexicans can effectively leverage these fiscal opportunities designed to ease their tax burdens and enhance their economic well-being.

Document Preview

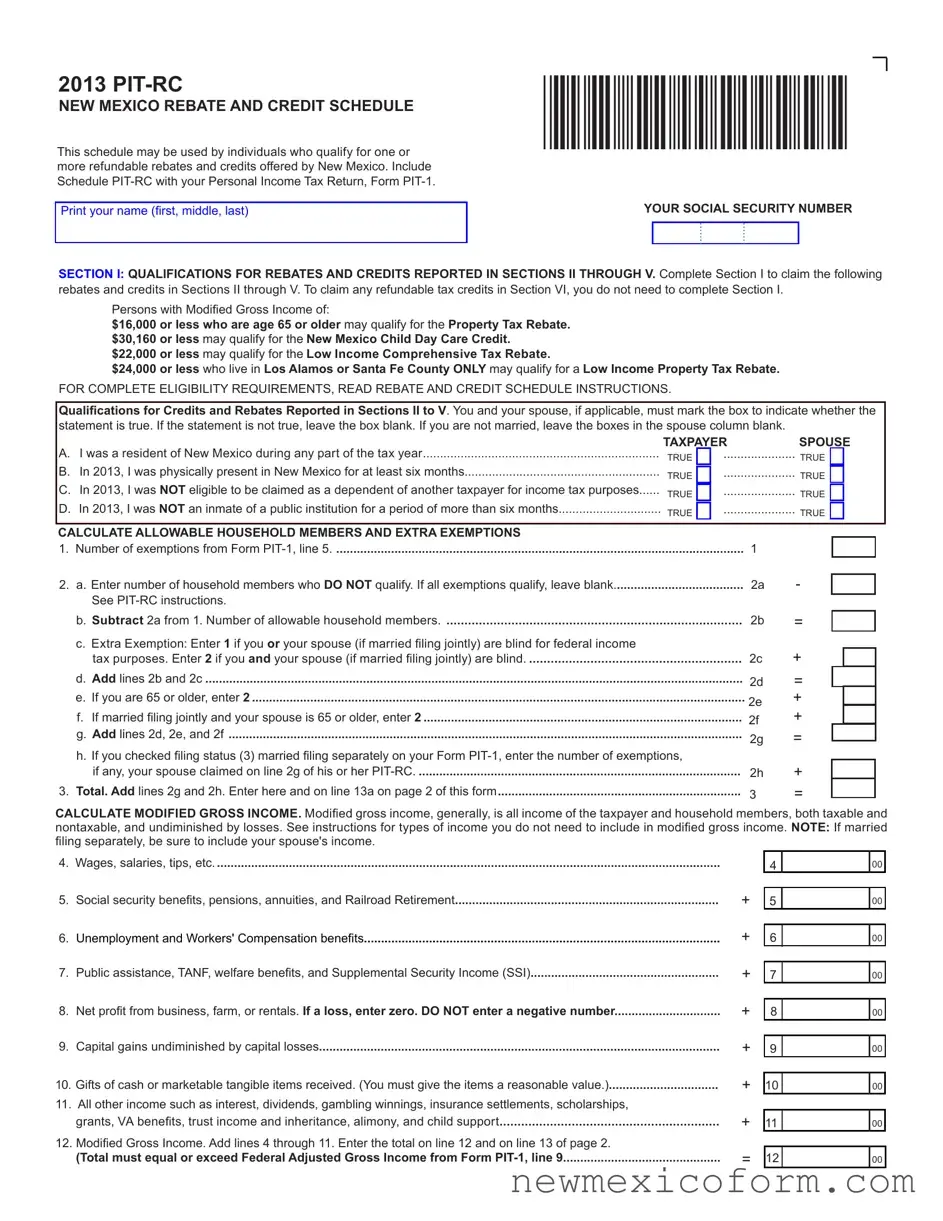

2013

NEW MEXICO REBATE AND CREDIT SCHEDULE

This schedule may be used by individuals who qualify for one or more refundable rebates and credits offered by New Mexico. Include Schedule

Print your name (irst, middle, last)

*130380200*

YOUR SOCIAL SECURITY NUMBER

SECTION I: QUALIFICATIONS FOR REBATES AND CREDITS REPORTED IN SECTIONS II THROUGH V. Complete Section I to claim the following rebates and credits in Sections II through V. To claim any refundable tax credits in Section VI, you do not need to complete Section I.

Persons with Modiied Gross Income of:

$16,000 or less who are age 65 or older may qualify for the Property Tax Rebate. $30,160 or less may qualify for the New Mexico Child Day Care Credit. $22,000 or less may qualify for the Low Income Comprehensive Tax Rebate.

$24,000 or less who live in Los Alamos or Santa Fe County ONLY may qualify for a Low Income Property Tax Rebate.

FOR COMPLETE ELIGIBILITY REQUIREMENTS, READ REBATE AND CREDIT SCHEDULE INSTRUCTIONS.

Qualiications for Credits and Rebates Reported in Sections II to V. You and your spouse, if applicable, must mark the box to indicate whether the statement is true. If the statement is not true, leave the box blank. If you are not married, leave the boxes in the spouse column blank.

A. I was a resident of New Mexico during any part of the tax year |

TAXPAYER |

SPOUSE |

||||

TRUE |

..................... TRUE |

|||||

B. In 2013, I was physically present in New Mexico for at least six months |

TRUE |

..................... TRUE |

||||

C. In 2013, I was NOT eligible to be claimed as a dependent of another taxpayer for income tax purposes |

TRUE |

..................... TRUE |

||||

D. In 2013, I was NOT an inmate of a public institution for a period of more than six months |

TRUE |

..................... TRUE |

||||

CALCULATE ALLOWABLE HOUSEHOLD MEMBERS AND EXTRA EXEMPTIONS |

|

|

|

|

|

|

1. |

Number of exemptions from Form |

1 |

|

|

|

|

2. |

a. Enter number of household members who DO NOT qualify. If all exemptions qualify, leave blank |

2a |

- |

|

|

|

|

|

|||||

|

See |

|

|

|

|

|

b. Subtract 2a from 1. Number of allowable household members |

2b |

c. Extra Exemption: Enter 1 if you or your spouse (if married iling jointly) are blind for federal income |

|

tax purposes. Enter 2 if you and your spouse (if married iling jointly) are blind |

2c |

d. Add lines 2b and 2c |

2d |

e. If you are 65 or older, enter 2 |

2e |

|

|

f. If married iling jointly and your spouse is 65 or older, enter 2 |

2f |

g. Add lines 2d, 2e, and 2f |

2g |

|

|

h. If you checked iling status (3) married iling separately on your Form |

|

if any, your spouse claimed on line 2g of his or her |

2h |

3. Total. Add lines 2g and 2h. Enter here and on line 13a on page 2 of this form |

3 |

=

+

=

+

+

=

+

=

CALCULATE MODIFIED GROSS INCOME. Modiied gross income, generally, is all income of the taxpayer and household members, both taxable and nontaxable, and undiminished by losses. See instructions for types of income you do not need to include in modiied gross income. NOTE: If married iling separately, be sure to include your spouse's income.

4. |

Wages, salaries, tips, etc |

|

5. |

Social security beneits, pensions, annuities, and Railroad Retirement |

+ |

6. |

Unemployment and Workers' Compensation beneits |

+ |

7. |

Public assistance, TANF, welfare beneits, and Supplemental Security Income (SSI) |

+ |

8. |

Net proit from business, farm, or rentals. If a loss, enter zero. DO NOT enter a negative number |

+ |

9. |

Capital gains undiminished by capital losses |

+ |

10. Gifts of cash or marketable tangible items received. (You must give the items a reasonable value.) |

+ |

|

11. All other income such as interest, dividends, gambling winnings, insurance settlements, scholarships, |

|

|

|

grants, VA beneits, trust income and inheritance, alimony, and child support |

+ |

12. |

Modiied Gross Income. Add lines 4 through 11. Enter the total on line 12 and on line 13 of page 2. |

|

|

(Total must equal or exceed Federal Adjusted Gross Income from Form |

= |

4 |

|

00 |

|

|

|

|

|

5 |

|

00 |

|

|

|

|

|

6 |

|

00 |

|

|

|

|

|

7 |

|

00 |

|

|

|

|

|

8 |

|

00 |

|

|

|

|

|

9 |

|

00 |

|

|

|

|

|

10 |

|

00 |

|

|

|

|

|

11 |

|

00 |

|

|

|

|

|

|

12 |

|

00 |

|

|

|

|

2013 |

*130390200* |

||

|

|||

NEW MEXICO REBATE AND CREDIT SCHEDULE |

|

||

YOUR SOCIAL SECURITY NUMBER |

|

||

|

|

|

|

|

|

|

|

SECTION II: LOW INCOME COMPREHENSIVE TAX REBATE (If line 13 is MORE than $22,000, DO NOT complete line 14.)

13.Enter Modiied Gross Income from line 12 ...............................................................................................................................

a. Enter Total Exemptions from line 3......................................................................................................................................

14.Low Income Comprehensive Tax Rebate. On Table 1 in the instructions, ind the Modiied Gross Income range that includes the amount on line 13, then move across to the column that matches the number of exemptions on

line 13a. Married couples iling separately must divide the result by two. .............................................................................

SECTION III: PROPERTY TAX REBATE FOR PERSONS 65 OR OLDER. (If line 13 is more than $16,000, DO NOT complete this section.)

15.PROPERTY OWNED. Tax billed for the calendar year on principal place of residence

16.PROPERTY RENTED

a. Amount of rent paid during the tax year for principal place of residence .......................................................................................................................................

b. If the amount entered on line 16a includes rent a government entity paid on your behalf, mark here |

16b |

c.Multiply line 16a by 0.06 and enter the amount here ....................................................................................................................

17.REBATE AMOUNT

a.Add lines 15 and 16c and then enter the total here............................................................................................................

b.Find the Modiied Gross Income range, on Table 2 in the instructions, that corresponds to the amount on line 13. Read across the table to the column showing your maximum property tax liability and enter the amount here.................

c.Property Tax Rebate. Subtract line 17b from 17a.

Do not enter more than $250 or if married iling separately, more than $125 ..............................................................................

SECTION IV: ADDITIONAL LOW INCOME PROPERTY TAX REBATE for Los Alamos or Santa Fe County |

18.LA |

|

residents only. (If line 13 is over $24,000, DO NOT complete this section.) |

||

18.SF |

18.REBATE AMOUNT

a.PROPERTY OWNED only. Tax billed for the calendar year on principal place of residence.............................................

b.Find the Modiied Gross Income range, on Table 3 in the instructions, that corresponds to the amount on line 13. Read across the table to the column showing your property tax rebate percentage and enter here..................................

c. Multiply line 18a by line 18b and enter here.

Do not enter more than $350 or if married iling separately, more than $175 .....................................................................

SECTION V: NEW MEXICO CHILD DAY CARE CREDIT. If Modiied Gross Income on line 13 is $30,160 or less, use the worksheet in the instructions to calculate your available Child Day Care Credit. Attach the worksheet and Forms

19. Enter either the total of Column G on the worksheet or $1,200, WHICHEVER IS LESS ........................................................

13 |

|

|

00 |

|

|

|

|

|

|

|

|

13a |

|

|

|

|

|

|

|

14 |

|

|

00 |

|

15 |

|

|

00 |

||||

|

|

|

|

|

|

|

|

16a |

|

|

00 |

||||

|

|

|

|

|

|

|

|

|

16c |

|

|

|

00 |

||

|

|

|

|

|

|

|

|

|

17a |

|

|

|

00 |

||

|

|

|

|

|

|

|

|

17b |

|

|

00 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

17c |

|

|

00 |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18a |

|

|

|

00 |

|

|

|

|

|

|

|

18b |

% |

|

|

|

|

|

|

18c |

|

|

00 |

|

19 |

|

00 |

20. |

Number of qualiied dependents under age 15 receiving child day care |

20 |

21. |

Enter the portion of the Federal Child Care Credit applied against your federal tax from Form 1040 or 1040A |

21 |

22. |

New Mexico child day care credit. Subtract line 21 from line 19. |

|

|

Married couples iling separately must divide the result by two |

22 |

SECTION VI: REFUNDABLE TAX CREDITS. |

|

|

23. |

Refundable medical care credit for persons 65 or older. See |

23 |

00

00

00

24.Special needs adopted child tax credit.........................................................................................................................

25.Renewable energy production tax credit. Attach Form

26.Refundable portion of the ilm production tax credit. Attach Form

SECTION VII: TOTAL REBATES AND CREDITS CLAIMED.

27. Add lines 14, 17c, 18c, 22, 23, 24, 25, and 26. Enter here and on Form

24

25

26

27

00

00

00

00

Document Properties

| Fact | Details |

|---|---|

| Form Number | PIT-RC |

| Year | 2013 |

| Title | NEW MEXICO REBATE AND CREDIT SCHEDULE |

| Purpose | Used by qualified individuals to claim refundable rebates and credits offered by New Mexico |

| Submission with | Personal Income Tax Return, Form PIT-1 |

| Qualification | Based on age, income, residency, and household composition |

| Income Thresholds | Vary for different credits and rebates (e.g., $16,000 for Property Tax Rebate for those 65 or older) |

| Special Conditions | Additional requirements for Los Alamos or Santa Fe County residents for certain rebates |

| Governing Law | New Mexico Taxation and Revenue Department regulations |

Steps to Filling Out New Mexico Pit Rc

Filing the New Mexico PIT-RC form is a step many residents take to claim various rebates and credits that the state offers. This process may seem intricate at first glance, but with proper guidance, it can be navigated with ease. The form itself is designed to accompany your Personal Income Tax Return, and it’s crucial for individuals who meet specific criteria based on age, income, and residency to maximize their potential refunds or reduce the amount owed. Detailed below are the steps to correctly fill out this form, ensuring that all applicable rebates and credits are claimed accurately.

- Print your full name and Social Security Number at the top of the form.

- In Section I: Qualifications, carefully read through each statement and mark the box as TRUE for each condition that applies to you and, if married, your spouse. Leave any irrelevant boxes unchecked.

- Calculate Allowable Household Members and Extra Exemptions:

- Enter the number of exemptions from Form PIT-1, line 5.

- For line 2a, note the number of household members who do not qualify, if any. If all qualify, leave blank. Deduct this number from the total exemptions to find the number of allowable household members (2b).

- If you or your spouse are blind, enter the appropriate number in 2c.

- Add up lines 2b and 2c for the total in 2d.

- For individuals 65 or over, make the relevant entries in lines 2e and 2f.

- Add lines 2d, 2e, and 2f for a total, then follow instructions for line 2h if filing status is married filing separately.

- Sum up lines 2g and 2h for the final count in line 3.

- Calculate Modified Gross Income by adding all reported income types listed from lines 4 through 11, noting the total on line 12. Include your spouse’s income if filing separately.

- In Section II, determine eligibility for the Low Income Comprehensive Tax Rebate by comparing your modified gross income and total exemptions, following instructions to calculate the rebate amount.

- For Sections III and IV, work through calculations regarding property tax rebates if you are 65 or older or living in specific counties, following instruction for owned or rented property.

- In Section V, calculate the New Mexico Child Day Care Credit using worksheet instructions and applicable forms regarding dependent care expenses.

- Verify any applicable Refundable Tax Credits in Section VI, including medical care for those 65 or older, special needs adoptive child, renewable energy, and film production credits, attaching necessary documentation.

- Total all calculated rebates and credits in Section VII and report this sum on your Form PIT-1, line 24.

Upon completing the form, ensure that all figures are accurate and all required attachments are included to avoid delays. It’s essential to review the form thoroughly before submission, ensuring that every applicable credit and rebate is claimed. This careful attention will maximize your potential benefits and contribute to a smoother processing of your tax return.

Frequently Asked Questions

What is the PIT-RC New Mexico Rebate and Credit Schedule?

The PIT-RC is a form used by individuals in New Mexico who qualify for refundable rebates and credits. It should be included with your Personal Income Tax Return, Form PIT-1. It allows eligible residents to claim various benefits, such as property tax rebates, child day care credits, and low-income comprehensive tax rebates.

Who needs to complete the PIT-RC form?

Individuals living in New Mexico during any part of the tax year who qualify for one or more of the refundable rebates and credits listed in Sections II through V of the form need to complete it. Additionally, if claiming any refundable tax credits in Section VI, completing Section I is not required. Qualifications are based on age, income levels, and residency in specific counties.

How do I know if I qualify for any of the rebates or credits on the PIT-RC form?

To determine eligibility for the rebates and credits:

- Review the qualifications in Section I related to your income, age, and residency.

- Check the specific income limits and ages required for each rebate or credit.

- For instance, individuals 65 or older with a Modified Gross Income of $16,000 or less may qualify for the Property Tax Rebate.

- Complete the required sections based on your eligibility as outlined in the PIT-RC instructions.

How is Modified Gross Income calculated for the PIT-RC form?

Modified Gross Income (MGI) includes all taxable and nontaxable income of the taxpayer and household members, minus any losses. To calculate MGI:

- Summarize wages, benefits, public assistance, net profit from business or rentals, gifts, and other incomes as specified in the form.

- Do not subtract losses or enter negative numbers for net profit losses.

- Ensure the total MGI is accurately reported on line 12 and matches or exceeds the Federal Adjusted Gross Income from Form PIT-1, line 9.

What should be done after completing the PIT-RC form?

After filling out the PIT-RC form based on your eligibility:

- Sum the amounts from Sections II through VI for all applicable rebates and credits you qualify for.

- Enter the total on line 27 of the PIT-RC form.

- Report this total also on Form PIT-1, line 24, to claim the rebates or credits against your personal income tax.

- Attach the PIT-RC schedule, along with any required worksheets or additional forms, to your Form PIT-1 when filing your tax return.

Common mistakes

Filling out forms can sometimes feel like navigating a maze. The New Mexico PIT-RC form, used by individuals to claim certain rebates and credits, is no exception. Paying close attention to detail can help avoid common pitfalls. To ensure you're on the right path, here are four mistakes to watch out for:

- Not Verifying Eligibility in Section I: It's vital to read and understand the eligibility requirements for rebates and credits listed in Section I thoroughly. This part of the form lays the groundwork by determining if you qualify for the benefits in Sections II through V. Skipping this step or assuming eligibility without verification can lead to incorrect claims and potential processing delays.

- Incorrectly Reporting Modified Gross Income: The calculation of Modified Gross Income (MGI) is central to the form. It includes all income, both taxable and nontaxable, without deductions for losses. A common error is not accurately tallying up all sources of income or mistakenly deducting losses, which skews the MGI figure. This misstep can affect eligibility for various rebates since many are income-based.

- Overlooking Specific Deductions and Rebates for Household Size and Age: When computing allowable household members and extra exemptions (2a through 2g), it's easy to overlook additional deductions for blindness or age. Even more, if you are 65 or older or have dependent children under age 15, there may be specific credits you're entitled to claim. Miscounting exemptions or failing to claim age-related rebates could lead to losing out on valuable benefits.

- Misunderstanding the County-Specific Credits: Residents of Los Alamos or Santa Fe Counties are eligible for an additional Low Income Property Tax Rebate if their income falls below a certain threshold. Not checking these specific conditions or missing the section entirely (Section IV) could mean missing out on extra benefits designed for residents of these areas.

Attention to detail and a careful review of the form's instructions can help avoid these common errors. Remember, each section of the New Mexico PIT-RC form is designed with a purpose, ensuring that individuals who qualify can benefit from the state's rebate and credit programs. By sidestepping these mistakes, you're not only making the process smoother but also maximizing your potential benefits.

Documents used along the form

When preparing New Mexico PIT-RC, the New Mexico Rebate and Credit Schedule, individuals often need to complement this form with several other documents to ensure accuracy in their submissions and to qualify for specific rebates and credits. These documents are essential for providing a comprehensive and precise tax return, ensuring individuals maximize their eligible returns while adhering to state requirements.

- Form PIT-1, New Mexico Personal Income Tax Return: This is the primary tax return form for New Mexico residents, where taxpayers report their income, deductions, and calculate the taxes owed. Form PIT-1 is essential as it provides the basis for eligibility and calculations on the PIT-RC form.

- Form PIT-CG, Caregiver's Statement: Required for those claiming the New Mexico Child Day Care Credit, this form verifies the child care expenses incurred, and it must accompany the PIT-RC when claiming this specific credit.

- Form RPD-41227, Renewable Energy Production Tax Credit Claim Form: Individuals claiming the Renewable Energy Production Tax Credit need to complete this form, providing details about their renewable energy systems and the energy produced. This form must be attached to the PIT-RC to validate the credit claim.

- Form RPD-41228, Application for Refundable Film Production Tax Credit: For individuals involved in film production eligible for state tax credits, this form outlines the expenses incurred and the applicable credits. It's required when claiming the refundable portion of the film production tax credit on the PIT-RC.

- Form RPD-41243, Statement of Withholding for Pass-Through Entity Owners: Relevant for individuals receiving income from pass-through entities, this form reports the state income tax withheld. It's necessary for accurately reporting income and taxes paid, which could affect the calculations on the PIT-RC.

Each of these documents plays a vital role in the completion of the New Mexico PIT-RC, ensuring individuals accurately report and maximize their eligibility for various state rebates and credits. It's crucial for individuals to thoroughly review and accurately complete each required form and attachment, as they collectively contribute to the individual's tax responsibilities and benefits under New Mexico law.

Similar forms

The New Mexico PIT-RC form, required for claiming various rebates and credits, exhibits similarities with other key documents like the Federal 1040 Schedule 3 and the state-specific PIT-1 form. These similarities arise from the forms' shared focus on facilitating the claim of credits and adjustments to income, albeit serving different specific functions within the spectrum of tax filing.

Firstly, the Federal 1040 Schedule 3 exhibits noticeable parallels with the New Mexico PIT-RC form in its structure and purpose. Both documents are designed to help taxpayers claim various credits and deductions that are not reported directly on the main income tax return forms. Schedule 3 of the Federal 1040 allows for the claiming of non-refundable credits such as the foreign tax credit, education credits, and general business credits. Like the PIT-RC, Schedule 3 requires taxpayers to detail qualifying expenses and information to correctly calculate and justify the credits being claimed. However, while the PIT-RC focuses on state-specific rebates and credits for New Mexico residents, Schedule 3 addresses credits recognized at the federal level.

Secondly, the New Mexico PIT-1 form, the state's main personal income tax return document, is another form with similarities to the PIT-RC. Where the PIT-1 form gathers general income, tax liability, and personal information necessary for computing state income tax, it also includes lines where totals from schedules like the PIT-RC are reported. This integration ensures the allowances calculated on the PIT-RC form effectively adjust the taxpayer's overall state tax liability. Both the PIT-1 and the PIT-RC form engage in a symbiotic relationship, with the PIT-RC serving as an essential supplement that directly impacts the calculations and outcomes determined on the PIT-1. This interconnectedness underscores the critical role specialized forms like the PIT-RC play in the broader context of tax filing and administration.

Dos and Don'ts

When completing the New Mexico PIT-RC form, it is crucial to follow specific guidelines to ensure an accurate and successful submission. Below is a list of dos and don’ts to assist with this process:

- Do read all instructions provided with the form carefully to understand the eligibility requirements for each rebate and credit.

- Do ensure that you include Schedule PIT-RC with your Personal Income Tax Return, Form PIT-1.

- Do print your name and provide your social security number at the top of the form as requested.

- Do accurately calculate your Modified Gross Income (MGI), as it impacts your eligibility for different rebates and credits.

- Do not fill out sections that do not apply to your eligibility status. If your MGI is above the threshold for a specific rebate, skip that part of the form.

- Do not enter a negative number for net profit from business, farm, or rentals; input zero if it results in a loss.

- Do not guess or approximate your income or expenses. Ensure all information is accurate and verifiable.

- Do not overlook the county of residence requirement for certain rebates such as the Low Income Property Tax Rebate available only to residents of Los Alamos or Santa Fe County.

By following these guidelines, you can confidently complete the New Mexico PIT-RC form, maximizing your potential rebates and credits while ensuring compliance with state tax laws.

Misconceptions

When it comes to filling out tax forms, especially those involving rebates and credits like the New Mexico PIT-RC form, misconceptions abound. Here are nine common misunderstandings:

- Misconception 1: You need to complete the entire form to claim any credit.

Actually, Section I needs to be completed only if you're claiming rebates and credits in Sections II through V. For refundable tax credits in Section VI, there's no need to fill out Section I.

- Misconception 2: Only those with very low incomes qualify for any rebates or credits.

While the form is designed to assist those with lower incomes, different sections of the form cater to various income levels up to $30,160, depending on the type of credit or rebate.

- Misconception 3: If you're not elderly, you won't qualify for any property tax rebate.

This isn't entirely true. Persons 65 or older with incomes of $16,000 or less may qualify for the Property Tax Rebate, but residents of Los Alamos or Santa Fe County with incomes of $24,000 or less may be eligible for a Low Income Property Tax Rebate regardless of age.

- Misconception 4: You can only claim the child day care credit if you have a low income.

Though the New Mexico Child Day Care Credit does have income restrictions, the cap is at $30,160, which accommodates a broader range of the middle class than some might expect.

- Misconception 5: Your modified gross income doesn't include non-taxable income.

Actually, the modified gross income calculation for this form generally includes all income, both taxable and non-taxable, without deductions for losses.

- Misconception 6: Married couples must file these credits together.

Married couples can claim applicable credits and rebates separately if they're filing separately, though they must follow specific instructions for dividing certain benefits.

- Misconception 7: You must itemize deductions on your federal return to claim these state credits.

There's no requirement on the form that ties state credit eligibility to whether you itemize deductions or take the standard deduction on your federal return.

- Misconception 8: The form is only for claiming credits for the current tax year.

The New Mexico PIT-RC form is designed for the specific tax year it references, in this case, 2013. However, the principles and structure of the form apply each year, although thresholds and requirements may be adjusted.

- Misconception 9: You cannot use the form if you're not a U.S. citizen.

Residency in New Mexico during the tax year, not citizenship, is the key requirement for eligibility for the rebates and credits listed.

Understanding these points can help ensure you accurately complete the New Mexico PIT-RC form and take advantage of the rebates and credits for which you're eligible.

Key takeaways

Navigating the New Mexico PIT-RC form can be an essential process for residents seeking to claim various state rebates and credits. Understanding the key elements of this form can help individuals maximize their potential benefits while ensuring compliance with state tax laws. Here are four key takeaways to guide you through filling out and using the New Mexico PIT-RC form effectively:

- Qualification Criteria: The form starts by outlining eligibility requirements for different rebates and credits based on factors such as age, income level, residency, and dependency status. For instance, individuals aged 65 or older with a Modified Gross Income (MGI) of $16,000 or less may qualify for a Property Tax Rebate. Additionally, different rebates apply to residents based on whether they live in specific counties like Los Alamos or Santa Fe. Understanding these criteria is crucial for determining which benefits you may be eligible for.

- Inclusion with Personal Income Tax Return: The PIT-RC form must be included with your New Mexico Personal Income Tax Return, Form PIT-1. This integration highlights the importance of the PIT-RC form in the broader context of your state tax filing, underscoring it as a vehicle through which to claim various rebates and credits that can potentially reduce your tax liability or increase your refund.

- Comprehensive Income Reporting: The form requires a detailed account of the filer's Modified Gross Income (MGI), encompassing various sources of income such as wages, benefits, and any other earnings. This comprehensive income reporting is instrumental in determining eligibility for the credits and rebates detailed in the form. Accurately reporting all income is not only a matter of legal compliance but also affects the calculation of potential rebates and credits.

- Documentation of Allowable Deductions and Exemptions: The PIT-RC form allows filers to calculate exemptions and deductions related to household members, age, and blindness status. These calculations directly impact the Modified Gross Income figure and, consequently, eligibility for various rebates and credits. Proper documentation and calculation in these sections can significantly affect your tax outcomes, potentially leading to greater rebates or reduced tax liability.

Thoroughly understanding and accurately completing the New Mexico PIT-RC form is essential for residents seeking to take advantage of state-offered tax rebates and credits. Taking careful note of eligibility requirements, accurately reporting income, and paying close attention to allowable deductions and exemptions are vital steps in maximizing potential benefits while ensuring compliance with New Mexico tax laws.

Common PDF Templates

New Mexico Courts - Gives structure to the often-daunting task of seeking redress through the courts, by delineating the essential components of a civil complaint in New Mexico.

New Mexico Llc Registration - Approval by the Town Clerk or designee marks the successful completion of the registration process, granting businesses official recognition by the community.