Fill Out a Valid Rpd 41359 New Mexico Template

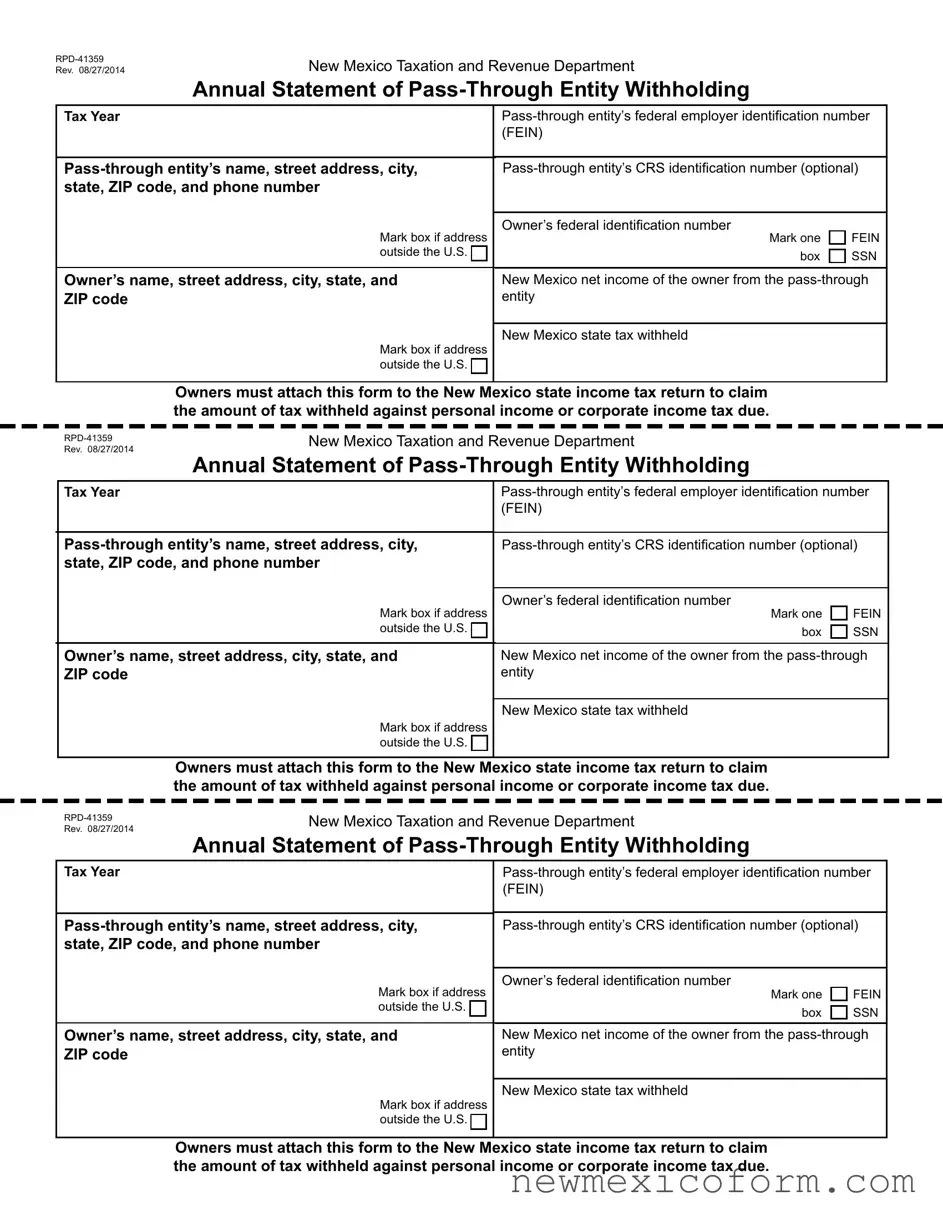

In navigating the complexities of tax obligations for pass-through entities in New Mexico, the RPD-41359 form emerges as a crucial document. This form, officially titled "Annual Statement of Pass-Through Entity Withholding," serves as a communication conduit between such entities and their owners, detailing each owner's share of New Mexico net income and the state tax withheld on their behalf for a given tax year. Designed by the New Mexico Taxation and Revenue Department and last revised on August 27, 2014, the form requires comprehensive information including the pass-through entity's (PTE's) federal employer identification number (FEIN), the entity and owner's detailed contact information, and specific financial details pertinent to income and tax withholdings. What makes RPD-41359 significant is its role in facilitating owners to claim the withheld tax amounts against their personal or corporate income tax dues, ensuring compliance with the Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act. Alongside its primary purpose, the form also accommodates entities operating across state or national borders, with provisions for marking addresses outside the United States. Understanding and accurately completing this form is pivotal for both pass-through entities and their owners to navigate the taxation landscape, comply with state laws, and accurately report and claim taxes in New Mexico.

Document Preview

New Mexico Taxation and Revenue Department

Annual Statement of

Tax Year |

|||

|

(FEIN) |

|

|

|

|

||

state, ZIP code, and phone number |

|

|

|

|

|

|

|

Mark box if address |

Owner’s federal identiication number |

Mark one |

FEIN |

outside the U.S. |

|

box |

SSN |

|

|

||

|

|

||

Owner’s name, street address, city, state, and |

New Mexico net income of the owner from the |

||

ZIP code |

entity |

|

|

|

|

|

|

Mark box if address |

New Mexico state tax withheld |

|

|

|

|

|

|

outside the U.S. |

|

|

|

|

|

|

|

Owners must attach this form to the New Mexico state income tax return to claim the amount of tax withheld against personal income or corporate income tax due.

New Mexico Taxation and Revenue Department

Annual Statement of

|

Tax Year |

||

|

|

(FEIN) |

|

|

|

|

|

|

|||

|

state, ZIP code, and phone number |

|

|

|

|

|

|

|

Mark box if address |

Owner’s federal identiication number |

|

|

Mark one |

FEIN |

|

|

outside the U.S. |

box |

SSN |

|

Owner’s name, street address, city, state, and |

New Mexico net income of the owner from the |

|

|

ZIP code |

entity |

|

|

|

|

|

|

|

New Mexico state tax withheld |

|

|

Mark box if address |

|

|

|

outside the U.S. |

|

|

|

|

|

|

Owners must attach this form to the New Mexico state income tax return to claim the amount of tax withheld against personal income or corporate income tax due.

New Mexico Taxation and Revenue Department

Annual Statement of

Tax Year |

|

||

|

|

(FEIN) |

|

|

|

|

|

|

|||

state, ZIP code, and phone number |

|

|

|

|

|

|

|

Mark box if address |

|

Owner’s federal identiication number |

|

|

Mark one |

FEIN |

|

outside the U.S. |

|

box |

SSN |

|

|

||

Owner’s name, street address, city, state, and |

|

New Mexico net income of the owner from the |

|

ZIP code |

|

entity |

|

|

|

|

|

Mark box if address |

|

New Mexico state tax withheld |

|

|

|

|

|

outside the U.S. |

|

|

|

|

|

|

|

Owners must attach this form to the New Mexico state income tax return to claim the amount of tax withheld against personal income or corporate income tax due.

New Mexico Taxation and Revenue Department

Annual Statement of

Instructions

page 1 of 2

About This Form.

cording to the Oil and Gas Proceeds and

NMSA 1978), are required to annually submit

Annual Statement of

use any of these three forms) to owners.

Owners (including partners, members, and beneiciaries,

which are all considered owners) must attach the forms received from PTEs to their New Mexico state income tax returnstoclaimtheamountofincomeandtaxwithheldagainst their personal income or corporate income tax due.

IMPORTANT: If no owners received net income from the

PTE for a calendar year, no ilings are required for that year.

An estate or trust that distributes New Mexico net income that is taxable to its recipients is a PTE and subject to

withholding pursuant to the Oil and Gas Proceeds and Pass- Through Entity Withholding Tax Act (Sections

An entity that has had tax withheld cannot pass a withholding statement directly to another taxpayer. Generally, the recipi- ent of the withholding statement must ile and report the tax

withheld on its New Mexico income tax return.

For Help. To get help with this form and corporate income taxes, in Santa Fe call (505)

help@state.nm.us.

INSTRUCTIONS FOR

This section is for PTEs. If you are an owner, see page 2,

Instructions for Owners.

What to File. To report the New Mexico net income and the state tax withheld for each owner, you are required to ile

Department and one of these forms to owners (any of these forms is acceptable):

•New Mexico Form

•Form

•A pro forma Form

If the net income you paid on Form

income from New Mexico and the amount of New Mexico tax withheld.

Other Reporting Requirements. PTEs are required to pro- vide suficient information to enable owners to comply with the

provisions of the Income Tax Act and the Corporate Income

and Franchise Tax Act, with respect to an owner’s share of

the net New Mexico income. A PTE that uses a Schedule

•New Mexico Form

•Form

•A pro forma Form

Due Date to Send Forms to Owners. Send the forms

the year for which you withheld New Mexico state tax from their net income. If February 15 falls on a Saturday, Sunday, or a state or national legal holiday, the return is timely if the postmark bears the date of the next business day.

How to Complete

Column 1

Year and Contact Information

1.Enter the tax year.

2.Enter your PTE name, address, and phone number. If the address is outside the U.S., mark the box.

3.Enter the owner’s name and address. If the address is outside the U.S., mark the box.

Column 2

Identiication Numbers, Net Income, and State Tax Withheld

1.Enter your PTE federal employer identiication number

(FEIN) using hyphens in

2.If applicable, enter the owner’s Combined Reporting System (CRS) identiication number using hyphens in

3.Enter the owner’s federal identiication number using hy- phens. If the number is an FEIN, enter it in

4.Enter the New Mexico net income the PTE allocated to the owner.

5.Enter the New Mexico state tax withheld.

New Mexico Taxation and Revenue Department

Annual Statement of

Instructions

page 2 of 2

Send Each Owner a Copy. After completing

(or Form

ForMoreInformation.See

INSTRUCTIONS FOR OWNERS

This section is for owners. If you are a PTE, see page 1,

Instructions for

Due Date to File with the State. You are required to ile the

How to File. Attach

income tax return when claiming the New Mexico income and the amount of tax withheld against your personal or corporate income tax due.

IMPORTANT:Unless you are listed as the owner or the recipi- ent of the income, do not attach these forms to your income tax return. When iling your return, you cannot use an income

and withholding statement that is issued to someone else.

Document Properties

| Fact | Detail |

|---|---|

| Form Name and Number | RPD-41359, Annual Statement of Pass-Through Entity Withholding |

| Revision Date | 08/27/2014 |

| Governing Law | Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act (Sections 7-3A-1 through 7-3A-9 NMSA 1978) |

| Purpose | Used by pass-through entities to report and withhold New Mexico tax from each owner's share of net income allocable to New Mexico. Owners attach this form to their New Mexico state income tax return to claim the amount of tax withheld. |

Steps to Filling Out Rpd 41359 New Mexico

Filling out the RPD-41359 form in New Mexico is essential for pass-through entities (PTEs) that distribute New Mexico net income to their owners, as it helps track the income and state tax withheld. It's an annual requirement, ensuring owners can accurately report their share of income and taxes withheld on their personal or corporate income tax returns. Here are the necessary steps for completing this form accurately.

- Enter the tax year at the top of the form to specify for which year you're reporting.

- In the section labeled "Pass-through entity’s information," input the entity's name, street address, city, state, ZIP code, and phone number. If the address is outside the U.S., make sure to mark the appropriate box.

- Provide the entity’s federal employer identification number (FEIN) in the designated field, using the format XX-XXXXXXX.

- If applicable, enter the pass-through entity's CRS identification number. Use hyphens in the format XX-XXXXXX-XXX.

- Next, fill in the owner’s information, including their name and address. Again, if the address is outside the United States, mark the corresponding box.

- For the owner's federal identification number, input either their Social Security Number (SSN) or FEIN, using the correct format (XXX-XX-XXXX for SSN or XX-XXXXXXX for FEIN) and checking the appropriate box to indicate which one you're using.

- Under the New Mexico net income and state tax withheld sections, enter the total net income allocated to the owner from the pass-through entity, followed by the amount of New Mexico state tax withheld from that income.

- Once all fields are filled in accurately, review the form for any errors or omissions. Correct any you find to ensure the information is reported correctly.

- Send a copy of the completed form to each owner by February 15 of the year following the year in which you withheld New Mexico state tax. If February 15 falls on a weekend or holiday, send it by the next business day.

After you've completed and distributed copies of the RPD-41359 form to all relevant owners, remember to keep a copy for your records. This documentation is crucial for both pass-through entities and their owners to ensure compliance with New Mexico's tax laws and to facilitate accurate income tax reporting. Should you or the owners need further assistance with the form or have specific questions regarding your tax obligations, the New Mexico Taxation and Revenue Department provides resources and contact information for guidance.

Frequently Asked Questions

What is the RPD-41359 form used for in New Mexico?

The RPD-41359 form is designed for pass-through entities in New Mexico to report and withhold state tax from each owner's share of net income that is allocable to New Mexico. This includes reporting for partners, members, or beneficiaries of these entities. The form serves to detail the New Mexico net income allocated to the owner and any state tax withheld, which owners must then attach to their New Mexico state income tax returns to claim against their personal or corporate income tax due.Who needs to file the RPD-41359?

Pass-through entities subject to the Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act that distribute New Mexico net income to their owners are required to file the RPD-41359. This includes entities such as partnerships, limited liability companies (LLCs), and S corporations that have New Mexico income allocable to their owners, as well as estates and trusts distributing taxable New Mexico net income to non-resident recipients.What are the alternatives to filing RPD-41359?

Instead of the RPD-41359, pass-through entities can file Form 1099-MISC or a pro forma Form 1099-MISC to report the New Mexico net income and the state tax withheld for each owner. These alternatives are acceptable for fulfilling the filing requirements under the New Mexico Taxation and Revenue Department guidelines.Is filing the RPD-41359 mandatory if no net income is distributed?

No, filing the RPD-41359 (or its alternatives such as Form 1099-MISC) is not required for a tax year if no owners received net income from the pass-through entity. The obligation to file only arises when there is distributable net income subject to New Mexico state tax.What information must be included on the RPD-41359?

When completing the RPD-41359, entities must include the tax year, the entity's name, address, phone number, and federal employer identification number (FEIN). Additionally, the owner's name, address, identification number (either SSN or FEIN), and the New Mexico net income allocated to the owner along with the amount of state tax withheld must be reported.When is the RPD-41359 due?

The completed forms (RPD-41359 or the alternative forms) must be sent to owners by February 15th of the year following the tax year in which the New Mexico state tax was withheld from their net income. If February 15th falls on a weekend or legal holiday, the deadline is extended to the next business day.How do owners use the RPD-41359?

Owners must attach the RPD-41359 form (or its alternatives) they receive from the pass-through entities to their New Mexico state income tax return. This allows them to claim the reported New Mexico income and the amount of tax withheld against their personal or corporate income taxes due.What should an owner do if they receive an RPD-41359 that is not in their name?

Owners should only use the RPD-41359 (or Form 1099-MISC or pro forma Form 1099-MISC) if they are the named owner or recipient of the income. If the form is not in their name, they should not attach it to their income tax return, as it cannot be used to claim income or withholding that has been reported for another individual or entity.Where can one get help with filling out the RPD-41359?

For assistance with the RPD-41359 form, individuals can contact the New Mexico Taxation and Revenue Department. In Santa Fe, the contact number is (505) 827-0825. There's also a toll-free number available, (866) 809-2335, with the option for corporate income taxes assistance. Emails can be sent to cit.taxreturn-help@state.nm.us for further help.

Common mistakes

Entering Incorrect Identification Numbers: A critical yet common mistake is the incorrect entry of identification numbers, including the pass-through entity’s Federal Employer Identification Number (FEIN) and the owner’s Social Security Number (SSN) or FEIN. These numbers should be thoroughly checked for accuracy. Hyphens are necessary in both FEIN (XX-XXXXXXX) and Social Security Numbers (XXX-XX-XXXX) to ensure proper formatting.

Failing to Report New Mexico Net Income Accurately: Another frequent error involves inaccurately reporting the New Mexico net income allocated to the owner from the pass-through entity. This figure must reflect the owner’s share of net income allocable to New Mexico accurately to ensure that tax liabilities are calculated correctly.

Omitting the CRS Identification Number When Applicable: While the Combined Reporting System (CRS) identification number is optional, it’s a mistake to omit this number if it’s applicable to the situation. Providing the CRS identification number, when relevant, facilitates the state’s processing of the form.

Neglecting to Mark the Address Outside the U.S. Box When Appropriate: Owners and entities with addresses outside the United States must mark the specific box indicating this status. This oversight can lead to errors in processing the form due to the unique handling required for international addresses.

Incorrectly Reporting New Mexico State Tax Withheld: Lastly, inaccurately reporting the amount of New Mexico state tax withheld is a mistake that can have significant implications. This amount should match the state tax withheld as recorded by the pass-through entity. Discrepancies here can affect the owner’s ability to claim the correct amount against their tax liabilities.

When it comes to the process of completing the RPD-41359, a form required by the New Mexico Taxation and Revenue Department for reporting and withholding tax on behalf of owners of pass-through entities, individuals often stumble upon a variety of common mistakes. Recognizing and avoiding these errors not only facilitates compliance with state tax regulations but also ensures the accuracy of reported financial information.

Understanding and addressing these common pitfalls can lead to a smoother and more accurate process for both pass-through entities and their owners. It’s essential for individuals involved in the completion of the RPD-41359 form to review their entries carefully and adhere to the detailed instructions provided by the New Mexico Taxation and Revenue Department to avoid these mistakes.

Documents used along the form

When preparing or reviewing documents related to the RPD-41359 in New Fexico, individuals and professionals often encounter a variety of other forms and documents that are necessary for comprehensive tax preparation and compliance. This includes both state-specific forms and federal documents that align with the requirements for pass-through entities and their owners. Here’s a brief overview of some pertinent documents:

- Schedule K-1 (Form 1065): Used by partnerships to report each partner's share of the partnership's earnings, losses, deductions, and credits to the IRS.

- Schedule K-1 (Form 1120-S): Similar to the partnership version, this is used by S corporations to report each shareholder's share of income, deductions, credits, etc., on their individual tax returns.

- Form 1099-MISC: Used to report miscellaneous income such as rents, royalties, medical and healthcare payments, and non-employee compensation.

- Form CRS-1: A New Mexico Taxation and Revenue form for reporting the gross receipts tax, compensating tax, withholding tax, and workers' compensation fee.

- New Mexico Form PIT-1: New Mexico Personal Income Tax Return, required for individuals to file taxes with the state.

- New Mexico CIT-1: New Mexico Corporate Income and Franchise Tax Return, used by corporations to file their state tax return.

- Form 1040: The standard federal individual income tax return form, which may include income or losses from pass-through entities.

- Form 1120: The U.S. Corporation Income Tax Return, which may be relevant for owners filing taxes as corporations.

Understanding the role and requirement of each document ensures proper tax preparation and compliance. Individuals and entities should carefully review their obligations, especially when dealing with multi-state operations or diverse income sources, ensuring all pertinent income and tax withholdings are accurately reported to both state and federal tax authorities.

Similar forms

The RPD-41359 New Mexico form is similar to the federal Form 1099-MISC in several ways. Both forms are intended to report income, although the specifics of the income and the context in which they are used vary. The Form 1099-MISC is commonly used by businesses to report payments made to non-employees, such as independent contractors, and covers a broad range of income types including rents, royalties, and non-employee compensation. The RPD-41359, conversely, is specifically designed for pass-through entities to report New Mexico state tax withheld from an owner's share of net income. Like the Form 1099-MISC, it requires identification numbers and information about the payer (in this case, the pass-through entity) and the recipient (the owner), as well as details about the income and tax withheld. Both forms play a crucial role in ensuring individuals and entities report their income accurately to the IRS and, for the RPD-41359, to the New Mexico Taxation and Revenue Department.

Another document similar to the RPD-41359 New Mexico form is the Schedule K-1. Used in the context of partnerships, S corporations, and certain trusts and estates, the Schedule K-1 documents the distribution of income, deductions, and credits to partners or shareholders. Like the RPD-41359, the Schedule K-1 is concerned with the allocation of income derived from a pass-through entity, though its scope is broader, encompassing not just income but also deductions and credits that affect a partner's or shareholder's taxable income. While the Schedule K-1 includes detailed information about the pass-through entity's income sources and financial activities, the RPD-41359 specifically focuses on the state tax withheld on behalf of the owner. The essential similarity lies in their function to report shareable income and withholdings from pass-through entities to their respective owners or beneficiaries, which is crucial for the preparation of individual tax returns.

Dos and Don'ts

When filling out the RPD 41359 New Mexico form, it's important to follow specific guidelines to ensure the process is completed correctly and effectively. This form is pivotal for pass-through entities in New Mexico, used to report and withhold state tax from an owner’s share of net income. To help with this process, here are ten dos and don'ts:

- Do verify the tax year at the top of the form to ensure you’re completing the form for the correct year.

- Do include the pass-through entity's name, address, and phone number, accurately reflecting the current information.

- Do enter the Federal Employer Identification Number (FEIN) of the pass-through entity using the correct format.

- Do complete the owner's information section with accurate details, including name and address. If the owner's address is outside the U.S., ensure to mark the relevant box.

- Do report the New Mexico net income allocated to the owner and the state tax withheld in the designated fields.

- Don't disregard the need to use hyphens in identification numbers such as the FEIN and the owner’s social security number or FEIN, which helps in maintaining the standard format required.

- Don't leave out the pass-through entity’s CRS identification number if it’s applicable. Even though it's optional, it can be crucial for record-keeping and verification processes.

- Don't send the form to the owners or the New Mexico Taxation and Revenue Department late. Ensure it's sent by February 15 of the year following the tax year in question or the next business day if February 15 falls on a weekend or holiday.

- Don't fill out the form inaccurately or incompletely. Double-check all information for accuracy before submission to avoid processing delays.

- Don't attach this form to the New Mexico state income tax return if you’re not the owner or the recipient of the income. This form should only be submitted by those who have received net income from the pass-through entity.

By adhering to these guidelines, the process of completing and submitting the RPD 41359 New Mexico form can be straightforward and mistake-free. This not only aids in the accurate reporting of income and tax withheld but also ensures compliance with New Mexico state tax obligations.

Misconceptions

Understanding the RPD-41359 form for New Mexico can sometimes be confusing, leading to misconceptions. This form is crucial for pass-through entities and their owners in New Mexico, presenting unique filing requirements and roles for all involved. Let's clarify some common misunderstandings:

- Misconception 1: Only entities with New Mexico income need to file the RPD-41359.

While it's true that the primary purpose of the RPD-41359 is to report New Mexico net income and the state tax withheld for owners of pass-through entities, it's a misconception that entities without New Mexico income are exempt from filing requirements. Even if no owners received net income from the entity for a calendar year, the entity might still have to comply with other reporting obligations under New Mexico law.

- Misconception 2: The form is only for entities formed in New Mexico.

Another common misunderstanding is that the RPD-41359 is exclusive to entities formed or based in New Mexico. In reality, any pass-through entity that allocates New Mexico net income to its owners, regardless of where it was formed, is required to submit this form. This ensures that New Mexico can accurately assess and collect taxes on income earned within the state.

- Misconception 3: Sole proprietors must also file the RPD-41359.

Sole proprietors might mistakenly think they need to file the RPD-41359. However, this form is specifically designed for pass-through entities like partnerships, S-corporations, and limited liability companies that have elected to be taxed as partnerships or S-corporations. Sole proprietors report their business income directly on their personal income tax returns, not through the RPD-41359.

- Misconception 4: Owners can file the form separately from their personal or corporate income tax returns.

Lastly, there's a misconception that owners receiving a completed RPD-41359 can file it separately from their personal or corporate income tax returns. However, owners must attach this form to their New Mexico state income tax return to properly claim the amount of tax withheld against the income tax due. This ensures the tax credits are correctly applied to the owner's overall tax liability.

Given these clarifications, it's imperative for both pass-through entities and their owners to understand the specific requirements and purposes of the RPD-41359 form to ensure compliance with New Mexico's tax laws and avoid unnecessary complications.

Key takeaways

Filing the RPD-41359 form in New Mexico for Annual Statement of Pass-Through Entity Withholding is a crucial task for both pass-through entities (PTEs) and their owners. It's designed to report and withhold New Mexico tax from each owner's share of net income allocable to New Mexico. Here are seven key takeaways to ensure compliance and accuracy in this process:

- The form is required by pass-through entities subject to the Oil and Gas Proceeds and Pass-Through Entity Withholding Tax Act to annually submit details of New Mexico income and tax withheld for each owner.

- PTEs can use the official New Mexico Form RPD-41359, Form 1139-MISC, or a pro forma Form 1099-MISC to report this information to both the owners and the New Mexico Taxation and Revenue Department.

- This statement is essential for owners, including partners, members, and beneficiaries, who must attach it to their New Mexico state income tax return to claim the amount of income and tax withheld.

- If no net income was distributed to the owners in a calendar year, the pass-through entity is not required to file for that year.

- To complete the form accurately, the PTE must include their Federal Employer Identification Number (FEIN) and, if applicable, the owner's Combined Reporting System (CRS) identification number, among other identification details and figures regarding net income and state tax withheld.

- PTEs are tasked with not only withholding and reporting state taxes but also providing sufficient information to enable owners to comply with their tax obligations under the Income Tax Act and the Corporate Income and Franchise Tax Act.

- The deadline for sending the completed forms to the owners is February 15 of the year following the tax year for which New Mexico state tax was withheld from their net income. If this date falls on a weekend or a state or national legal holiday, the next business day is considered the due date.

Fulfilling these requirements diligently not only ensures compliance with New Mexico state tax laws but also streamlines the process of claiming tax withholdings for both pass-through entities and their owners. It is a pivotal step in managing the tax responsibilities that come with generating income within New Mexico.

Common PDF Templates

Nm State Tax Refund - For refunds related to boat or vehicle-related payments, such as incorrect fee applications, the Form is designed to facilitate your request efficiently.

New Mexico Llc Taxes - Businesses can indicate if they are part of a unitary group on this form.

New Mexico Filing Requirements for Non Residents - Employers are required to list any equipment, materials, or chemicals involved in the accident or exposure.